Investing prudently is the best way to grow money over time. So whether you are planning to begin with ₹10,000 or ₹1 lakh in 2025, knowing how the returns compound can guide you through select investment options.

Fixed deposits, recurring deposits, mutual funds, and small savings schemes have varied returns over time with their tenure and risk. Knowing your investment’s potential value helps everybody plan better for achieving his financial goals.

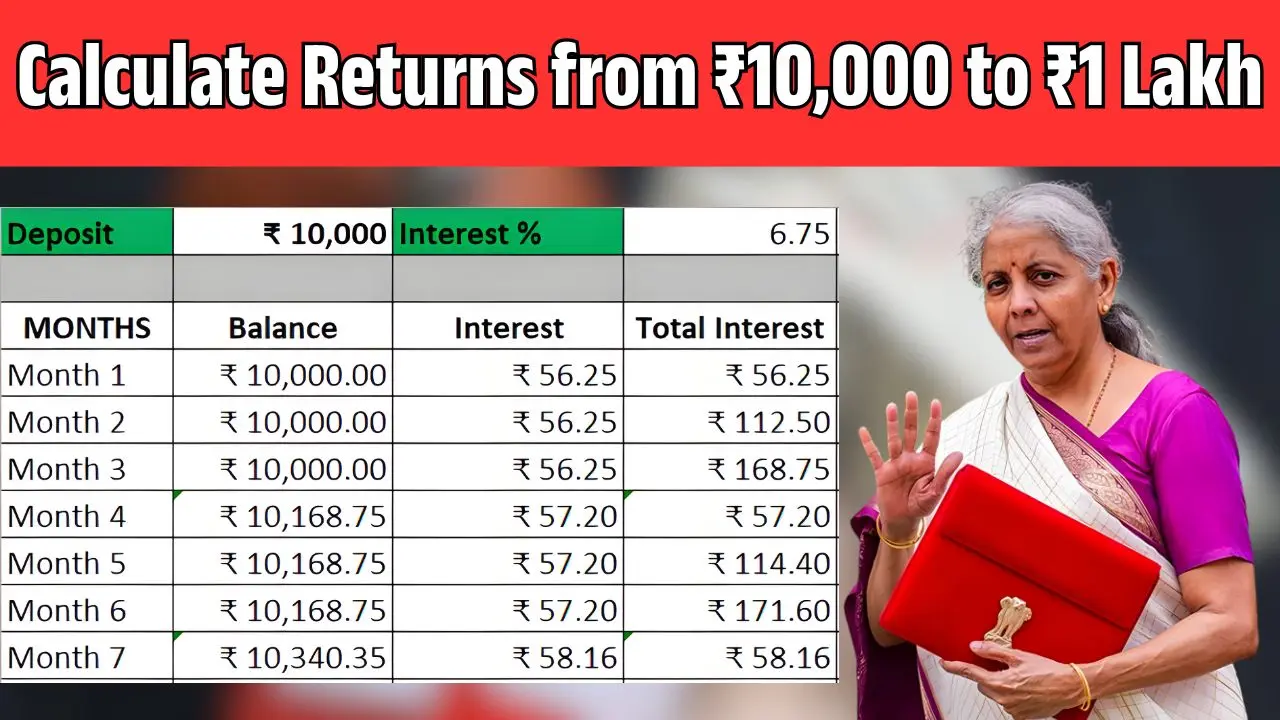

How Returns Are Calculated

The growth potential of any investment could be described based on three basic factors – initial investment, interest rate and tenure. If we consider general products like fixed deposits or schemes of the post-office, where returns are known, one can directly expect what has to be given out.

For market-linked returns of mutual funds, the return is directly linked to the market, i.e., relating to the equity share market. The returns could be boosted over the long term, although they could offset growth in the short term. Compound interest helps highly over the time period: interest is treated as an investment to trigger additional earnings.

Estimated Returns with Different Investments

Calculating returns for ₹10,000, ₹25,000, ₹50,000 even ₹1 lac, it becomes very straightforward to observe the growth. Out of any such configuration, one case could be, for example, an annualized growth of 7 percent leading ₹10,000 to approximately ₹10,700 in one year.

Similarly, ₹50,000 equals around ₹53,500 and ₹1 lac gets close to ₹1.07 lac. What do you benefit more for the highest compounding? For example, just assuming if you get annual compounding and thus you may go up to ₹1.23 lac after 3 years.

Choosing Wish Investment

Several types of investors work best with various financial products. Fixed deposits and the post office schemes for safety-conscious and guatanteed benefit investors. Mutual Funds are better for those who can afford to take on a certain amount of market volatility in return for potentially better returns. Novices generally go with small SIPs for getting some taste of the long-term growth.

Conclusion

It does not matter whether you are investing ₹10,000 or ₹1 Lakh-the most important thing is comprehending how returns actually mount up in small instalments over a period. Once you have an approximate figure figured out, you can then set the level of expectation and plan for the roadmap of opting for investment opportunities. With a decent plan, even a small amount committed now can see many more zeroes by the year 2025 with the power of compounding.

Also Read: Canara Bank FD Scheme: Invest RS 1 Lakh And Earn Guaranteed RS 39,750 Interest